The Strategy or Means

Now, take some time to consider the future financial needs of your child based on the planning assumptions you had made earlier. Adapted from templates used by Special Needs Trust Company (SNTC), the categories of needs captured in the table below may also be a helpful reference:

| Category of Needs | Examples | |

| 1 | Basic Daily Living | Food, groceries, meals, transport, handphone subscription, internet subscription, personal grooming |

| 2 | Healthcare | Health screening, medical consultations, dental treatment, rehabilitation and therapy, fitness |

| 3 | Other Therapy and Support Services | Programme fees (e.g., day activity centre), vocation and employment training |

| 4 | Housing | Rental / Mortgage, housekeeping, home maintenance |

| 5 | Personal Development & Upgrading | Skills upgrading courses, enrichment |

| 6 | Social & Recreation | Special occasions, entertainment, personal devices, vacations, special interest activities |

| 7 | Others | Insurance premiums |

With these in mind, you can now consider options for your financial plan.

For Goal #1: Set aside money to support your child’s future expenses

Example options:

- Save a fixed amount each month and earmark it for your child’s future expenses

- Purchase endowment polices to build up a pool of savings over a fixed term.

- Invest a portion of your net worth at the prevailing inflation rate over the years

- Increase your income stream to increase the sum of money available for your child, e.g., renting out a spare room in your flat, identifying a sustainable side hustle or gig work, etc.

- Consider pledges of support from family members

- If possible, develop your child’s strengths such that he may be able to earn an income

For Goal #2: Make sure that the money is safely given to your child

Example options:

- Provide a sum of money to someone you trust who can give your child a fixed allowance as long as he lives.

- Create a trust (through a trust company or Special Needs Trust Company) that pays your child a monthly allowance from the assets that you leave behind.

- Tap on the Special Needs Savings Scheme (SNSS) that provides a monthly payment to your child from your CPF fund until the funds run out.

- Buy insurance policies that provide monthly payouts to your child over his lifetime.

Every financial plan is unique. What goes into the financial plan for your child depends on your situation. There are different options you can use to put together your financial plan to meet the 2 goals. Your plan may consist of just one or a combination of these components: trust, bank account, insurance policies, Special Needs Saving Scheme (SNSS) account, etc.

You can find out more information about these options below. This will enable you to determine what combination of these options is suitable for you and your child.

📝 Lasting Power of Attorney

The Lasting Power of Attorney (LPA) is a legal document which allows you to appoint one or more persons to make decisions and act on your behalf if you lose mental capacity one day.

Making an LPA allows you to choose who you wish to make decisions on your behalf should you lost mental capacity one day. It also means that your loved ones do not have to apply to court for a deputyship order, which can be costly and time-consuming.

To complete the LPA process, you will be required to pay and engage an LPA Certificate Issuer (typically a doctor or a lawyer) to witness and certify your LPA.

📜 A Trust

A trust is a legal arrangement that allows you (known as the settlor) to place your assets so that an appointed trustee can administer and manage them for your Child’s benefit.

Why set up a Trust?

- Safeguard your Child's welfare and financial security.

- Rely on a Trustee who is well-informed about the rights of persons with special needs.

- When you want to avoid placing the legal and financial responsibilities of managing the money on relatives or friends.

- When you foresee that relatives or friends may move away, suffer ill health and cannot commit to the long-term management of the financial affairs of your Child.

- Rely on a permanent professional body to manage and administer your money for your Child.

You can visit a commercial Trust company to set up a Trust. Alternatively, you can do so with the Special Needs Trust Company (SNTC), which is Singapore’s only non-profit Trust company.

✍️ A Will

A Will is a written document that sets out your instructions and wishes on how you want your estate (your money, property, possessions, and other assets) to be distributed after your death. To make a Will, you should consider engaging a lawyer.

If you are unable to afford private legal services, you can consider visiting the Legal Aid Bureau. The Legal Aid Bureau provides legal advice and assistance to persons with limited means, subject to their means testing criteria.

Alternatively, you may wish to visit The Law Society of Singapore’s listing of lawyers who practise Community Law.

🧑⚖️ Making a CPF Nomination

Regular Nomination

When you make a CPF Nomination, your CPF savings will be distributed to the person you nominate in a lump sum payment.

You can make an appointment to visit any CPF Service Centre and complete the CPF Nomination Form in the presence of the Customer Service Executives.

Any new nomination you make will supersede your earlier nomination.

SNSS Nomination

Alternatively, you can also consider making a nomination under the CPF Special Needs Savings Scheme (SNSS). Under the SNSS, the nominating parents can nominate their Children with special needs to receive fixed monthly disbursements from their CPF savings after the parents' demise until the funds run out. CPF savings will be distributed to your nominated child on a monthly basis. You can determine the amount of monthly payouts for your nominated child. The minimum payout will be $250 per month, with a minimum duration of at least one year.

If your child is below 18, the disbursement will be made to the legal guardian or the court-appointed deputy (if the child has one).

To make a nomination under the SNSS, you may wish to contact the Special Needs Trust Company (SNTC).

📄 Insurance Policies

Life Insurance is a contract between an insurance policy holder and an insurance company, where the insurer promises to pay a sum of money in exchange for a premium, upon the death of an insured person, total permanent disability or after a set period.

👨👩👧 Testamentary Guardian (if your child is under 21 years old)

There are 2 types of legal guardians:

- A natural guardian

- A testamentary guardian

A natural guardian is the surviving parent of the children. On the other hand, a testamentary guardian need not be biologically related to your children and is appointed in a will.

Section 7 of the Guardianship of Infants Act (GIA) entitles parents to appoint any person to be a testamentary guardian for their children.

Why is a Testamentary Guardian necessary?

In the unfortunate event of your death, it is advisable to ensure that your children receive the care and protection that you would like them to have. This may be done through the appointment of a testamentary guardian.

A testamentary guardian is a person who legally steps into your shoes after your death. He or she will take care of your children in your stead. The testamentary guardian will also have custody over your children.

This means that he or she will have the power to make decisions affecting the welfare of your children until they reach 21 years of age. These decisions may range from the basic provision of food, clothing, and shelter to the fulfilment of your children’s emotional and educational needs.

A testamentary guardian is appointed during the drafting (or amendment) of your will. You should seek legal advice to draft/amend your Will.

⚖️ Deputyship Application (if your child is over 21 years old)

A deputy is appointed by the court to make certain decisions on behalf of a person who lacks mental capacity. A deputy can be an individual or a licensed trust company under the Trust Companies Act (Cap.336), as prescribed by the Mental Capacity Regulations.

Parents of children with disabilities may apply to the court to appoint themselves as deputies for their Children and another person as a successor deputy. A successor deputy will take over for you to make decision for your child, in the event that you yourself become unable to.

If your Child is enrolled in a Special Education school, or is enrolled in an MSF-funded Day Actvity Centre/Sheltered Workshop, you may be able to receive assistance with your deputyship application under the Assisted Deputyship Application Programme.

Please contact your Child’s school or SG Enable to receive guidance under the programme.

What will your strategy be?

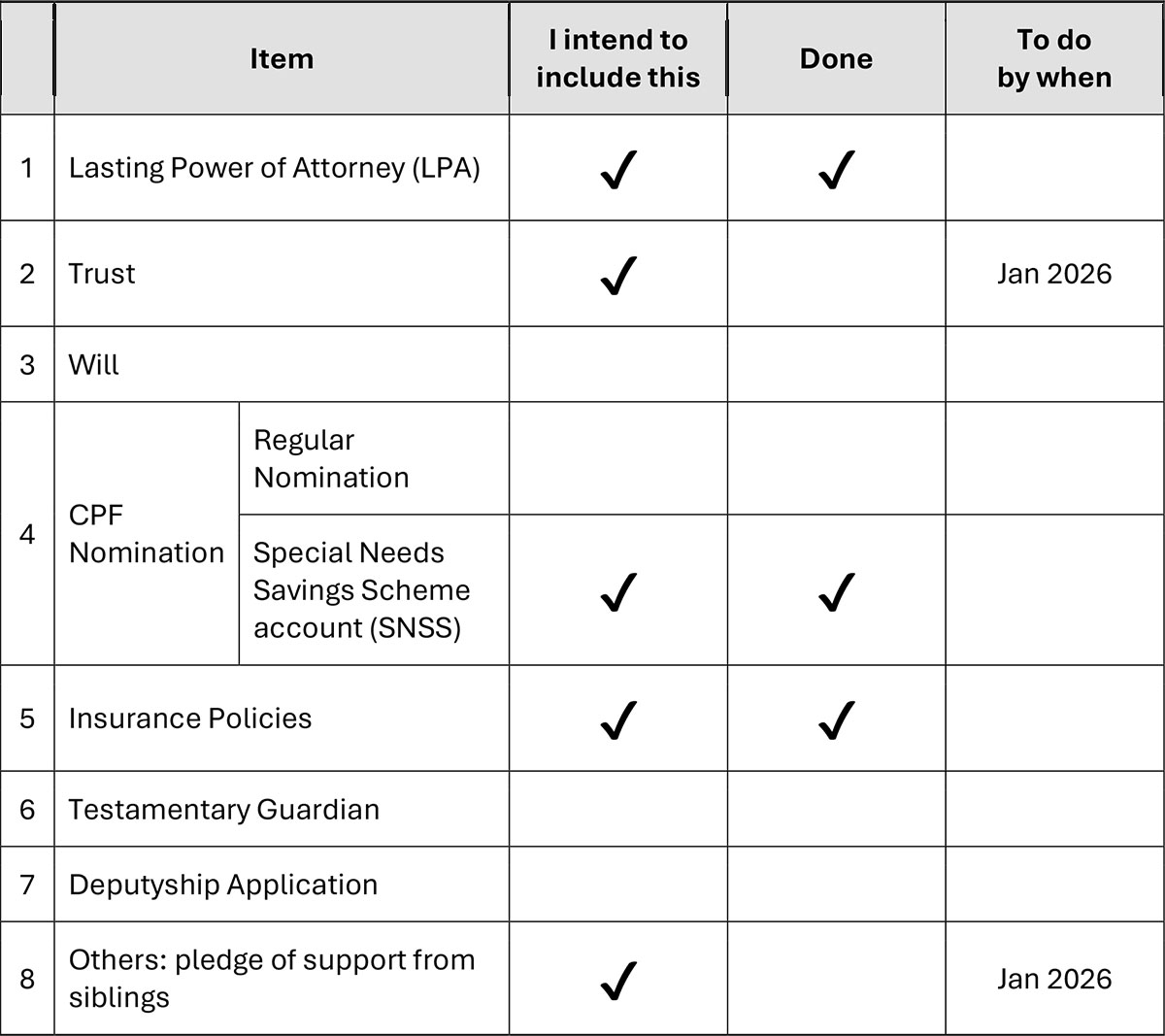

Activity: Options for Your Financial Plan

Identify the items you intend to include in your financial plan by checking the appropriate boxes. If you have already started working on a financial plan for your child, you can also think through what else you may need to do to make it complete.

Example for Jon’s Family